Rate-Cuts or You're Cut

Hello All,

It’s been a relatively quieter week in terms of economic data as inflation data has mostly been relatively tame whereas hard-data / soft-data has continued to come in better than expected & the bigger headline of the week has been the speculations of Trump looking to fire Powell (trial balloon) which has thus far been denied & as the week has generally progressed, so has breadth & the indices have snapped higher on the week as both Spooz & the Q’s went on to make yet another new ATH whereas the Dow is the laggard on the week although still sits higher by 36bps.

In April, we wrote about hard assets & the structural framework behind hard assets given recent events & future outlook along with some historical perspective as well… you can check it out below for those whom may have missed… it’s been pretty spot on.

Hard Assets in an Era of Soft Money

As global central banks quietly rearm their stimulus arsenals and fiscal deficits spiral past the point of discipline, the foundations of the global monetary order are beginning to crack. Amid this shift, one question looms larger than ever: Are we on the verge of a new commodity supercycle?

We also published the follow up educational piece which has been highly requested and majority of the topics covered were all suggested by you all, so I hope you find good benefit.

For those who may have missed, a link to Educational Piece Part: Deux can be found here.

For those who may have missed the first educational piece, I included the range of topics covered below along with a link to the piece for those who would like to go back and read:

- General background / knowledge on all option strategies

- In-depth talk on risk / reversals & how to go about expressing / utilizing them

- Options Structuring

- When to used naked calls / puts vs. spreads

- Choosing expiration dates

- Identifying key pivots / supports / resistance zones

- General briefing on stock gaps

- What to look for in regards to fundamentals

- Implementing fundamental / macro / technicals into a trade

- Hedging

- Creating risk/reward setups

- Taking profits / managing losses

- Overall Process

- Book recommendations

A link to the first educational write-up can be found here.

- SPY

To waste no time & jump right into Spooz, well, yet another new ATH was achieved today as each & every dip continues to remain shallow & bought. As we’ll discuss a bit later, but yesterday specifically, we did see Spooz flush lower following the speculations that Trump was looking to fire Powell, which then Trump came out to then deny the rumors thus Spooz & the general indices paired back the losses… a pretty clear ‘trial balloon’ by the administration… similar to the one from April in which rumors circulated the administration was looking to issue a 90-day pause which then was denied but shortly following, sure enough the administration ended up implementing the 90-day delay tariff pause.

Now, more specifically in regard to the indices but earlier on in the week, we did have poor breadth across the board but these last couple of days have shown quite the improvement which has led the % of Stocks Above the 20D to rebound to 62% thus signaling a market that continues to remain generally healthy in terms of broader participation & in the shorter-term, isn’t necessary overly extended to the upside either given action within the indices has been more grindy whereas individual names have more so taken over in terms of upside vol.

Now, in regard to Spooz but following todays upside move, again, Spooz in itself went on to achieve a new ATH above 6300 but ended up closing out the day just below 6300. We don’t have much data in terms of significance tomorrow & next week is relatively quieter as well & really in the shorter-term, the bigger event risks looming is the August 1st deadline in terms of trade-deals / tariffs expected to be implemented & then the other looming potential risk being the firing of Powell, again, we’ll talk more on this subject later.

With Spooz having closed just below 6300, again, 6300ish is where bears have tried to make a stance in terms of selling pressure as Spooz has now consolidated for over 2-weeks just below 6300 but has failed to firm up above in each instance… the clear LIS for bears in terms of trying to protect against further upside remains (6290 / 6300ish), but if we were to see Spooz see followthrough to the upside & emerge out of this near 3-week consolidation to the upside, there isn’t necessarily much stopping Spooz from seeing range expansion upwards toward the 6400 / 6500ish range above.. especially considering hard-data has continued to hold in much better than feared & inflation data thus far has been more tame than expected as well (granted, next month will be more important in terms of nail in the coffin in respect to tariffs impacting inflation data or not).

On the flip side, if we were to see Spooz once again reject near 6300ish, I do think we could see Spooz maybe go on to get a firm test of the 20d below near 6200ish (maybe driven by sell-the-news ERs season & or headline volatility), but ultimately, I continue to think the interim LIS remains around 6175 / 6145ish below (Coincides with 20d & Prior ATHs) & as long as that general area does remain supportive, do think in the interim that bulls will maintain their current edge / dips will continue to remain shallow & bought whereas if we were to see Spooz rollover further / prior ATHs fail to come in as support, I could see Spooz rolling over further towards 6050ish (assuming prior ATHs fails to come in as support) which essentially coincides with the Ceasefire bull-gap established a few weeks back & in general, I do think the prior range before this recent breakout to new highs (6050 / 5950ish) will likely serve as a medium-term broader support, whilst important MAs (200d / 50d / 100d) sit just below as well for added confluence, and will continue to keep indices more bifurcated in the medium-term / dips will continue to be shallow as long as that supportive confluence remains… and of course the other added factor to keep in mind is that many Individuals / HFs / PMs have been itching for any sort of dip to ‘let them in’ to this market so barring a surprise shock (still maintain that hard-data rolling over > tariff headlines), do think that dips will still likely continue to get bought until proven otherwise.

In terms of economic data, there is a bit to discuss & in general, data has been very positive this week. In respect to inflation data, as we discussed on Tuesday but headline CPI came inline whereas Core came in slightly softer than expected… the one worry was the rise in goods inflation & without the decline in auto, Core would’ve posted quite the surge in June… nevertheless, as we mentioned earlier but inflation data will essentially boil down to next month in terms of whether or not we’re seeing any material impacts from tariffs or not, as thus far, it’s been non-apparent in data.

Yesterday, carrying on with inflation data but we had PPI #’s which came in softer than expected & every single economist missed the #… it’s a good thing thats what they get paid to do! Nevertheless, the more interesting factor to pay attention to with PPI #’s is the PPI components that feed through PCE & as shown below, airfare posted quite the decline whereas health services have continued to remain sticky… overall, not much signal but the report in general was better than what was expected.

Now, here’s where things start to get interesting… the July Philly Fed data was a BLOWOUT report… the Mfg. Index jumped to +15.9 vs. -1.0 est. & -4.0 prior & Employment rose +10.3 vs. -9.8 prior… a goldilocks report all around & not recessionary at all.

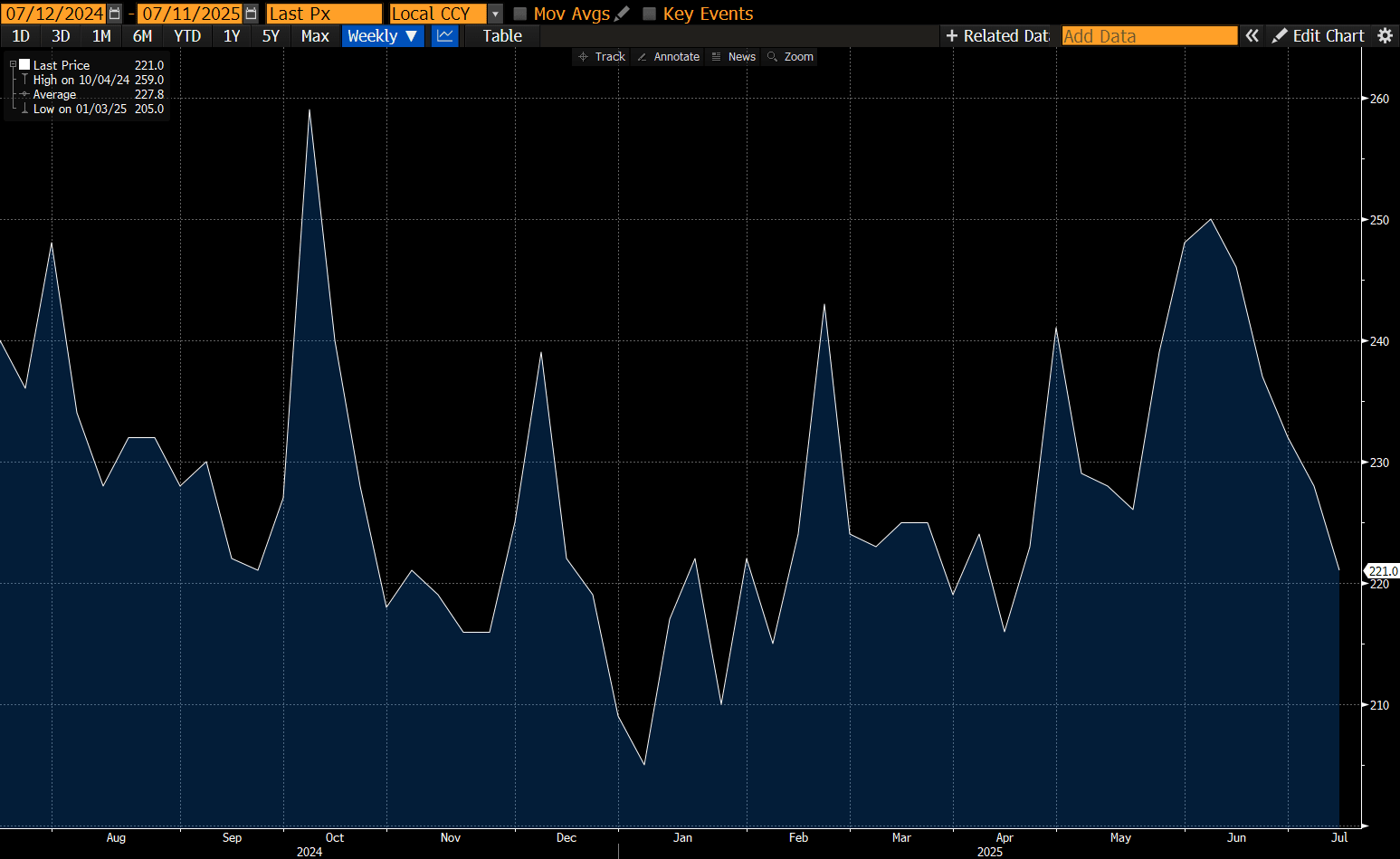

The other standout datapoint is jobless claims posted another declining week & have now retreated back towards 221k after being near 250k just a few weeks back. Whilst many started to slightly panic on jobless claims a few weeks back, we held firm with our opinion that the rise was specifically due to seasonality & sure enough, the prior spike higher in jobless claims has fully retraced… turns out it was a nothing-burger after all, shocker.

And lastly, retail sales posted a strong beat today & the biggest standout was the rise in control group, 0.5% & it’s important as control group feeds through directly into GDP… another added datapoint that hard-data in general continues to hold in much better than feared. After-all, who could’ve seen this coming... oh wait, we did!